How to Contribute $77,000+ to Roth Accounts Even With High Income

Turn today’s earnings into tomorrow’s tax-free fortune.

How to Contribute $77,000+ to Roth Accounts Even With High Income

Think you make too much money to contribute to Roth accounts? Think again! This common misconception stops thousands of high earners from accessing one of the most powerful retirement savings tools available. The truth is, there are several smart strategies that let you build tax-free wealth for retirement, no matter how much you earn.

The Big Myth That's Costing You Money

Here's what many people believe: "If I make over $165,000 as a single person (or $246,000 as a married couple), I can't use Roth accounts at all."

This is completely wrong! While it's true that direct Roth IRA contributions have income limits, there are multiple ways around these restrictions. Smart high earners use what we call "backdoor" strategies to get their money into tax-free Roth accounts.

What Makes Roth Accounts So Special?

Before we dive into the strategies, let's talk about why Roth accounts are such a big deal:

- Tax-free growth forever: Once your money is in a Roth account, it grows without Uncle Sam taking a cut. Ever.

- Tax-free withdrawals in retirement: When you're 59½ or older, you can take money out without paying taxes on any of it.

- No required minimum distributions: Unlike traditional retirement accounts, Roth IRAs don't force you to take money out when you turn 73.

- More flexibility: You can withdraw your contributions (not earnings) anytime without penalties after the account has been open for five years.

Strategy #1: The Backdoor Roth IRA

The Backdoor Roth IRA is probably the most popular strategy for high earners. Here's how it works in simple terms:

The Three-Step Process

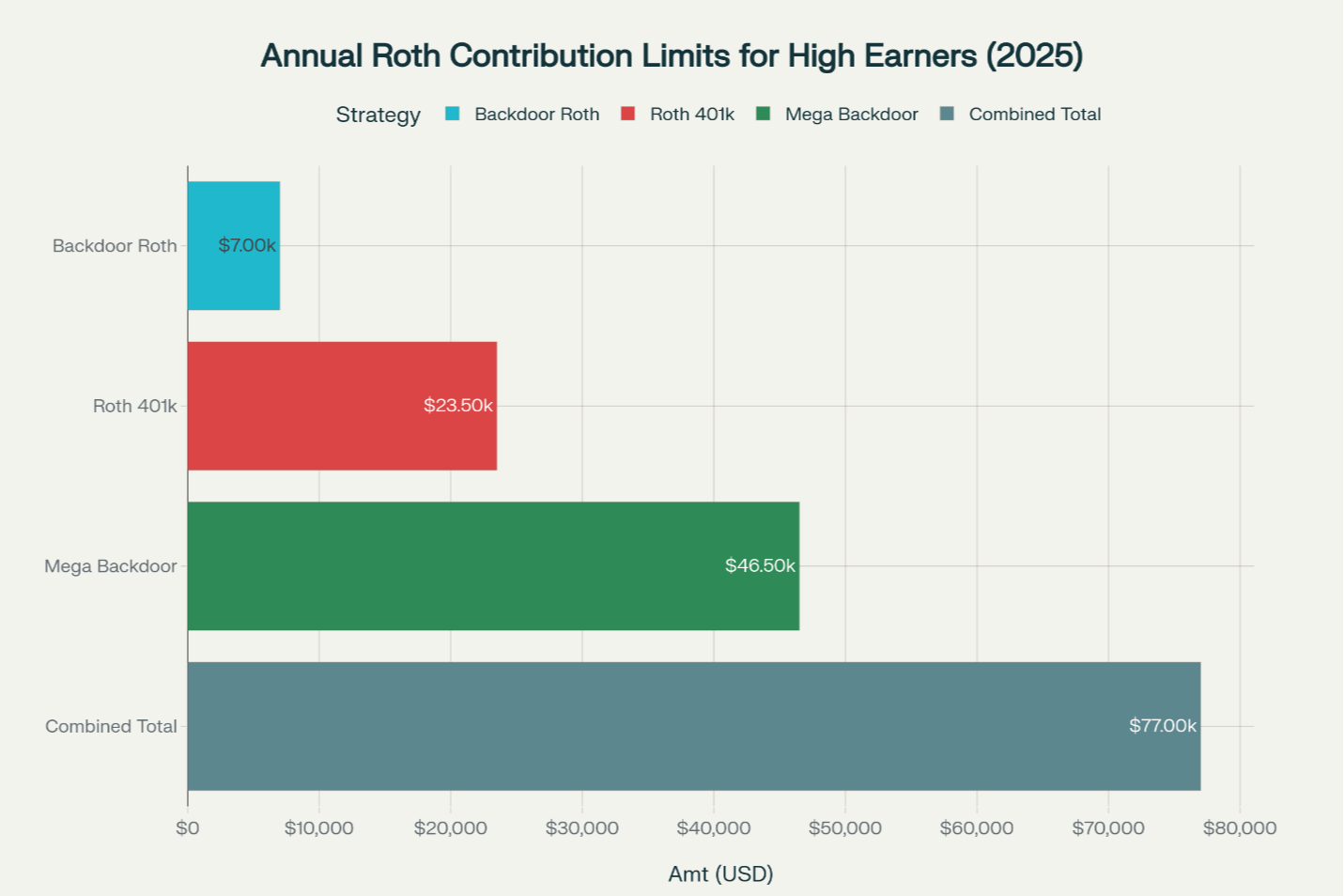

- Put money into a traditional IRA (up to $7,000 in 2025, or $8,000 if you're 50 or older).

- Immediately convert that money to a Roth IRA

- File Form 8606 with your tax return each year. This memorializes that your contribution in step one is classified as a “Non-Deductible” Contribution

Since there are no income limits on IRA conversions, this strategy works for everyone, regardless of how much you make.

Important Things to Know

The Pro-Rata Rule: If you already have money in traditional IRAs from previous years, this strategy gets more complicated. You can't just convert the "new" money - the IRS makes you convert proportionally from all your traditional IRA accounts.

Tax implications: If you do this correctly with no existing traditional IRA balances, there should be minimal taxes owed, potentially none at all.

Timing matters: Most experts recommend converting the money as soon as possible after making the contribution to avoid any investment gains that would be taxable.

Strategy #2: Roth 401(k) Contributions

Here's some great news: Roth 401(k) accounts have NO income limits at all. If your employer offers this option, you can contribute directly without any backdoor strategies.

2025 Contribution Limits

- Under age 50: $23,500

- Age 50-59 and 64+: $31,000 (includes $7,500 catch-up)

- Age 60-63: $34,750 (includes new $11,250 super catch-up)

The beauty of Roth 401(k)s is their simplicity. You just tell your payroll department how much you want to contribute, and it comes out of your paycheck after taxes.

Strategy #3: The Mega Backdoor Roth

This is where things get really exciting for high earners. The Mega Backdoor Roth can let you put an additional $46,500 into Roth accounts in 2025.

How It Works

- Max out your regular 401(k) contributions ($23,500 in 2025)

- Make after-tax contributions to your 401(k) beyond the normal limit

- Convert those after-tax contributions to either a Roth IRA or Roth 401(k)

The Requirements

Not everyone can do this strategy. Your employer's 401(k) plan must allow:

- After-tax contributions beyond the normal limits

- Either in-service withdrawals or in-plan Roth conversions

The Math

The total 401(k) contribution limit for 2025 is $70,000 (or $77,500 if you're 50+). Here's how it could break down:

- Your regular contributions: $23,500

- Employer match: $5,000 (example)

- Available for after-tax contributions: $41,500

Real-Life Case Study: Meet Sarah, The Smart High Earner

Let's look at how these strategies work in the real world.

Sarah's situation:

- Age: 35

- Income: $200,000 (single)

- Goal: Maximize tax-free retirement savings

What Sarah can't do: Contribute directly to a Roth IRA (her income is too high)

What Sarah can do in 2025:

- Backdoor Roth IRA: $7,000

- Roth 401(k) at work: $23,500

- Mega Backdoor Roth (if her plan allows): Up to $41,500 additional (Sarah receives a $5,000 Match)

Total potential Roth savings: Up to $72,000 per year!

Common Mistakes to Avoid

- Mistake #1: Waiting too long to convert in a Backdoor Roth

Convert your traditional IRA to Roth as soon as possible after making the contribution. - Mistake #2: Forgetting about existing traditional IRA balances

The pro-rata rule can create unexpected taxes if you have old traditional IRA money. - Mistake #3: Not checking if your 401(k) allows after-tax contributions

Many people assume their plan doesn't allow this without actually asking. - Mistake #4: Paying conversion taxes from retirement accounts

Always pay taxes on conversions from outside money when possible.

Getting Started: Your Action Plan

Step 1: Check your current situation

- What's your income for 2025?

- Do you have existing traditional IRA balances?

- Does your employer offer Roth 401(k) options?

Step 2: Talk to your HR department

- Ask if your 401(k) plan allows after-tax contributions

- Find out if in-service withdrawals or in-plan conversions are available

Step 3: Meet with a financial professional

- Review your specific tax situation

- Create a multi-year Roth conversion strategy

- Make sure you’re following all IRS rules correctly

Step 4: Set up automatic contributions

- Backdoor Roth IRA contributions can be done annually

- Roth 401(k) contributions come directly from payroll

- Mega Backdoor Roth conversions might be done quarterly or monthly

The Bottom Line

Don't let the "Income is too high" myth stop you from building tax-free wealth. High earners actually have more Roth options than most people realize. With the right strategies, you could potentially contribute $77,000 or more to Roth accounts in 2025.

The key is understanding your options and creating a plan that works for your specific situation. These strategies can be complex, so working with a qualified financial advisor is usually worth the investment.

Remember, tax laws change, and everyone's situation is different. What works great for one high earner might not be the best choice for another. The important thing is to stop believing you can't use Roth accounts and start exploring which strategies make sense for you.